Beyond… Death and Taxes

In dealing with risks in projects we find ourselves doing things like: risk identification… meaning we sit around a table and ask each other “what went wrong last time?” …for sure there are better ways to do risk identification. Ways which actually increase the chances of finding those risks which will actually mean something. However, before we even start touching on so called “best practices”, I would like to stop a second on a more basic topic which relates to understanding what we are actually talking about when we utter the word: risk.

In dealing with risks in projects we find ourselves doing things like: risk identification… meaning we sit around a table and ask each other “what went wrong last time?” …for sure there are better ways to do risk identification. Ways which actually increase the chances of finding those risks which will actually mean something. However, before we even start touching on so called “best practices”, I would like to stop a second on a more basic topic which relates to understanding what we are actually talking about when we utter the word: risk.

What is a risk? That which might happen but is uncertain… OK.

What is uncertain? The best way to answer that question may be to first figure out what, on the other hand, is NOT uncertain (and therefore would characterize not risks, but facts).

According to Franklin, “In this world nothing can be said to be certain, except death and taxes.“ (Benjamin Franklin, 1706-90, letter to Jean-Baptiste Leroy, 1789 – re-printed in The Works of Benjamin Franklin, 1817). I know nobody asked me, but at least in this matter, I happen to agree with him. Think of any project element which will occur in the future. Are you really sure that… the vendor will deliver according to those lead times? Or that installations will meet the quality we have had in the past? Or that the acceptance will be based solely on that contract? Or that the… and the list goes on.

No! Of course you are not sure. But we need to start somewhere to build our plans (I can nearly hear you saying this) if we question everything we will never even start! True. Those however are not called facts, but assumptions.

We need to accept the fact that our decisions, plans, dreams, visions (read: whatever is in the future), are based on assumptions, and therefore on uncertainty. Did you like certainty? Too bad, forget about it, it doesn’t exist.

So the real question is, if only death (and taxes) are certain… what do we do with all the rest?

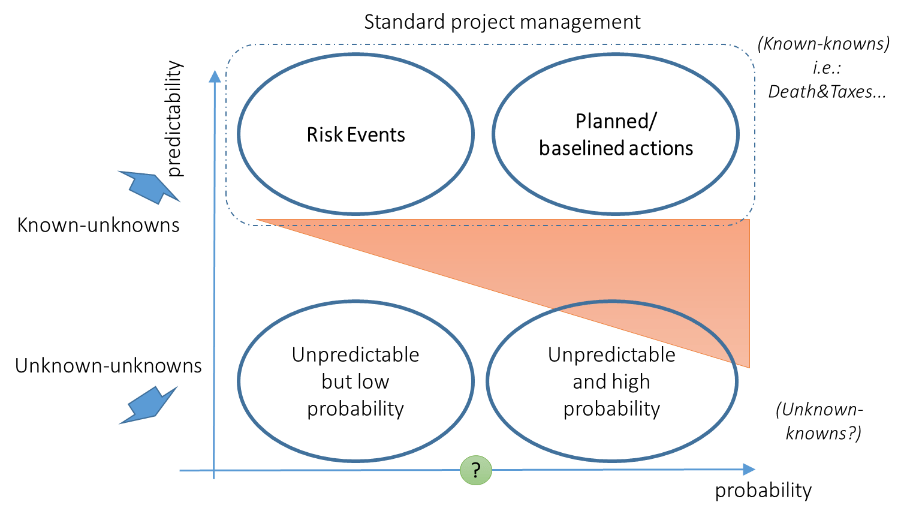

Take a look at this picture:

The top part, the known-unknowns, are what we deal with in normal project management. You may see them separated out in this second picture below.

If the probability is high enough we consider them facts and plug them into our project plan, if the probability is lower than “enough” we might do “risk management” and put them into a risk register. We decide which is which (the split) based on what we defined as: “the probability is high enough…”. That is pretty vague.

These two figures are trying to tell at least two basic things:

- The split between what we deal with as risks in projects and what we deal with as facts, is actually subjective and based on assumptions and on our personal/corporate risk tolerance levels.

- We are not looking at the whole bottom part of the picture (i.e.: the unknown-unknowns). Practically not at all. In the best cases we create some sort of percentage allocation for “unexpected events”.

In reality there are ways to deal with both these points. You have probably heard the expression: “Risk management is actually project management for grown-ups”. Acknowledging our over-reliance on the so called “illusion of certainty”, may be a start, and may help us in getting beyond dealing only with certainties: death… and taxes.

Cheers!

Max